Investment Flows, Deal Tracker, and Financial Benchmarks

Tracking $100B+ in committed capital — from PE stakes to hyperscaler mega-projects.

Live capital-markets context: day-ahead power price (key opex input) · grid carbon intensity (RE100 capex driver). Cross-link to /data-centres · /insights · renewable-finance API guide.

India's DC Sector Attracted More Capital in 2025 Than in the Preceding Five Years Combined

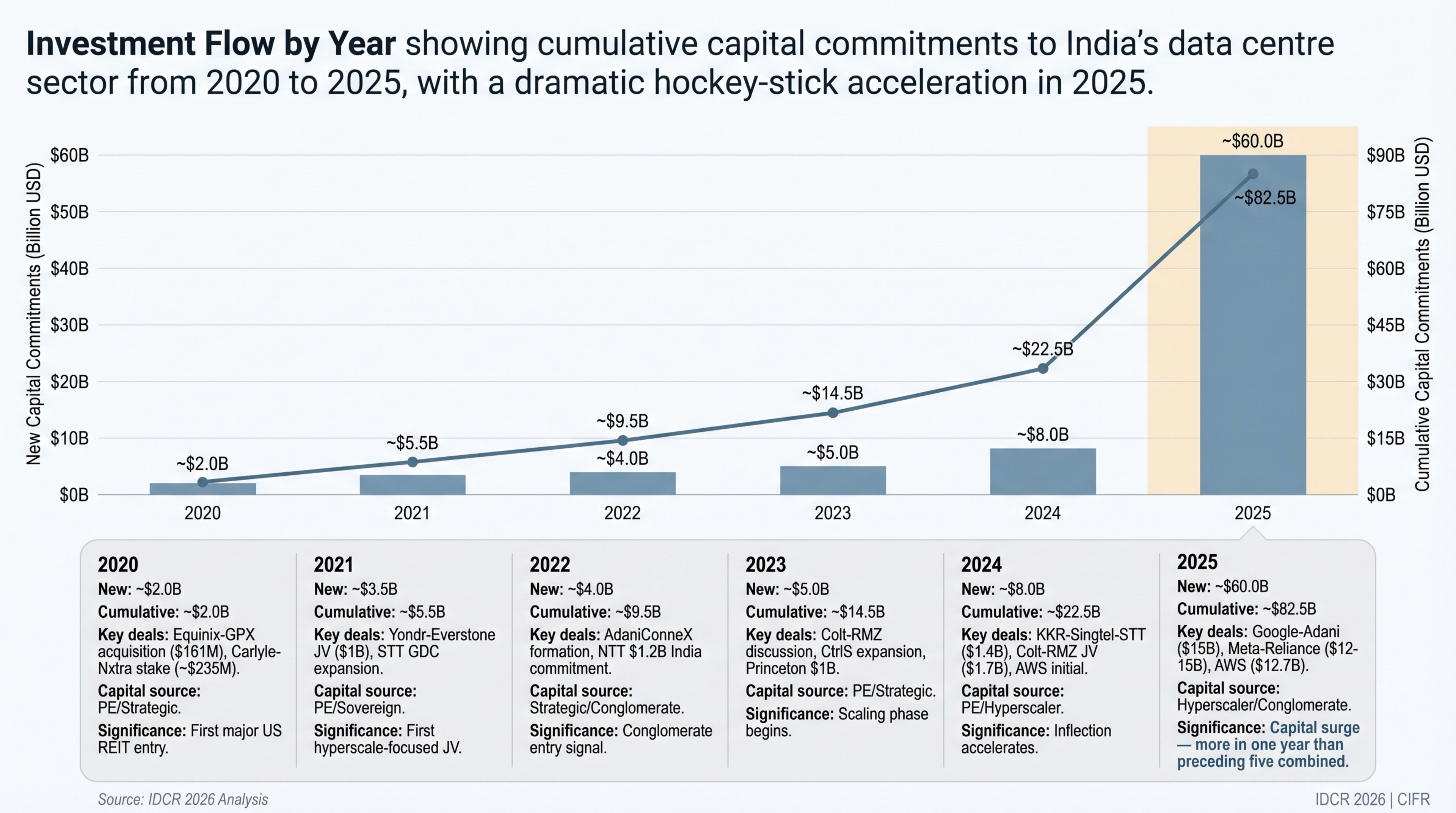

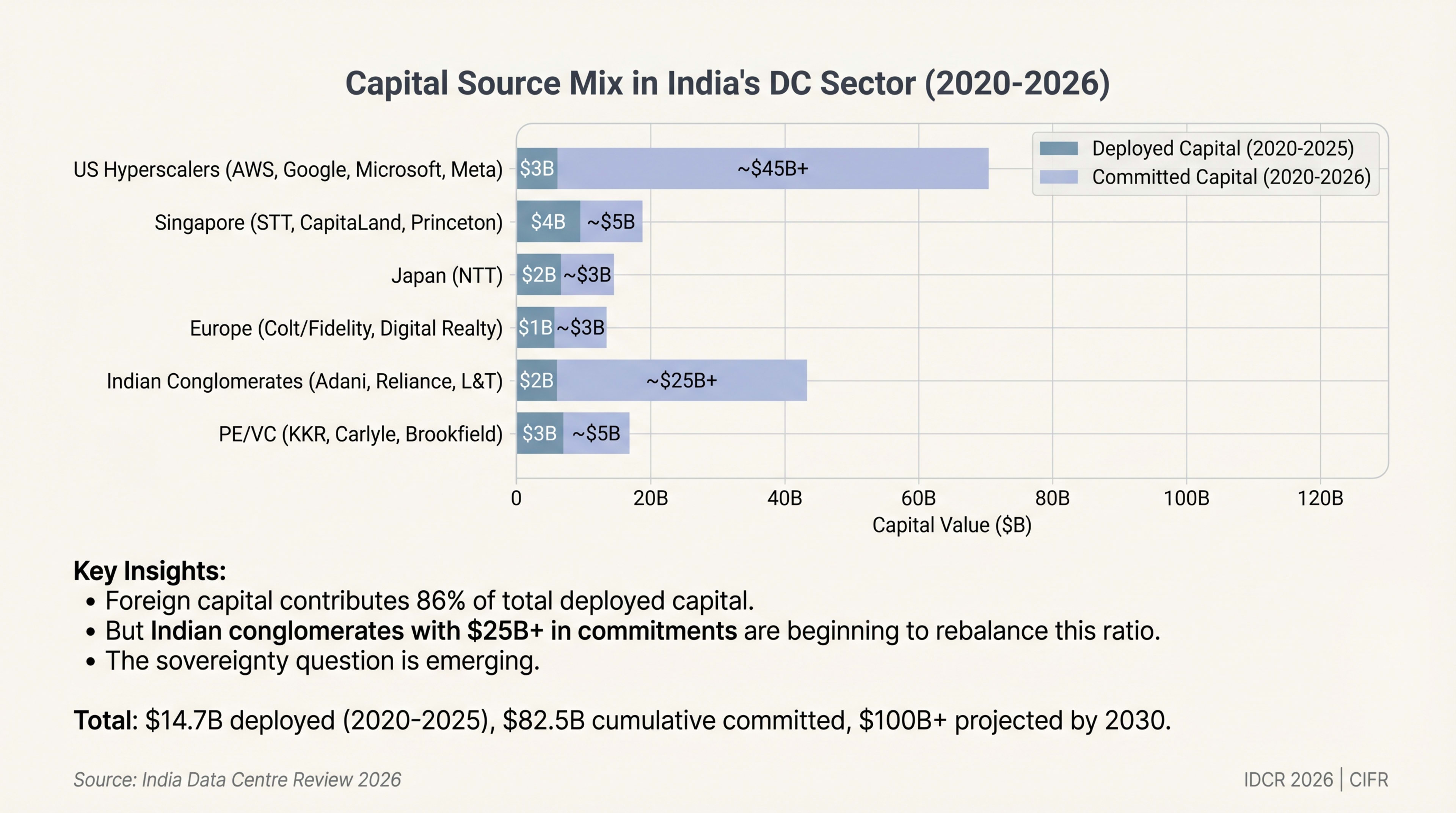

India's data centre sector crossed an inflection point in 2025. Roughly $56.4 billion was deployed in 2025 alone — more than the entire cumulative deployment of the prior five years combined (Global DC Hub Q1 2026· Global DC Hub2026) — bringing cumulative committed capital to ~$126 B. Foreign institutional investors contributed approximately 86% of deployed capital through 2024 (Houlihan Lokey· Houlihan LokeyDec 2025); the 2025 conglomerate wave (Adani, Reliance, L&T) is rebalancing the ratio. Data centres rank as a nationally significant infrastructure category, explicitly referenced in the Union Budget 2026-27 as critical digital infrastructure eligible for infrastructure lending rates and accelerated depreciation.

This structural shift reflects global confidence in India's digital infrastructure thesis. Hyperscalers and conglomerates committing $10B+ to captive and joint-venture builds signal capital maturation beyond traditional real estate financing models.

| Investment Flow by Year (Cumulative Commitments) | |||||

|---|---|---|---|---|---|

| Year | New ($B) | Cumulative ($B) | Key Deals | Capital Source | Significance |

| 2020 | $2.0 | $2.0 | Equinix-GPX ($161M); Carlyle-Nxtra ( $235M) | PE/Strategic | First major US REIT entry |

| 2021 | $3.5 | $5.5 | Yondr-Everstone JV ($1B); STT GDC expansion | PE/Sovereign | First hyperscale-focused JV |

| 2022 | $4.0 | $9.5 | AdaniConneX formation; NTT $1.2B India commitment | Strategic/Conglomerate | Conglomerate entry signal |

| 2023 | $5.0 | $14.5 | Colt-RMZ discussion; CtrlS expansion; Princeton $1B | PE/Strategic | Scaling phase begins |

| 2024 | $8.0 | $22.5 | KKR-Singtel-STT ($1.4B); Colt-RMZ JV ($1.7B); AWS initial | PE/Hyperscaler | Inflection accelerates |

| 2025 | $60.0 | $82.5 | Google-Adani ($15B); Meta-Reliance ($12-15B); AWS ($12.7B) | Hyperscaler/Conglomerate | Capital surge |

Source: Houlihan Lokey Dec 2025; Bloomberg; CNBC; company press releases; IDCR 2026 estimates

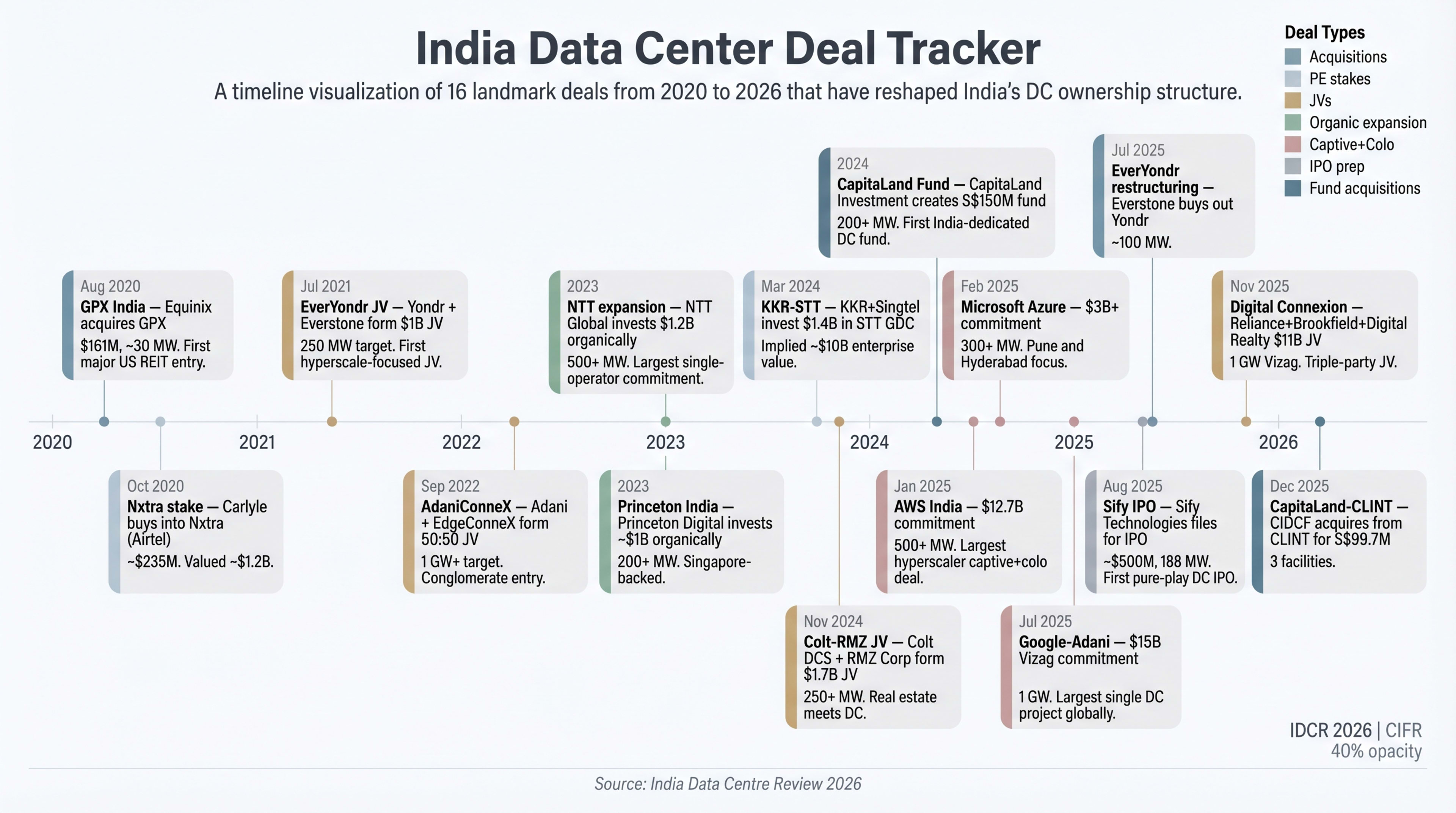

Landmark Deals Reshaped India's Data Centre Ownership Structure

Sixteen major transactions between 2020 and 2026 shifted control from dispersed regional operators to integrated platforms combining captive hyperscaler infrastructure with colocation revenue streams.

| India Data Center Deal Tracker (2020-2026) | |||||||

|---|---|---|---|---|---|---|---|

| # | Date | Deal | Parties | Value | Type | MW | Significance |

| 1 | Aug 2020 | GPX India | Equinix ← GPX | $161M | Acquisition | 30 MW | First major US REIT entry |

| 2 | Oct 2020 | Nxtra stake | Carlyle → Nxtra (Airtel) | $235M | PE stake | N/A | Valued $1.2B |

| 3 | Jul 2021 | EverYondr JV | Yondr + Everstone | $1B | JV | 250 MW | Hyperscale-focused JV |

| 4 | Sep 2022 | AdaniConneX | Adani + EdgeConneX | Undisclosed | 50:50 JV | 1 GW+ | Conglomerate entry |

| 5 | 2023 | NTT expansion | NTT Global | $1.2B | Organic | 500+ MW | Largest single-operator |

| 6 | 2023 | Princeton India | Princeton Digital | $1B | Organic | 200+ MW | Singapore-backed |

| 7 | Mar 2024 | KKR-STT | KKR+Singtel → STT GDC | $1.4B | PE stake | N/A | Implied $10B EV |

| 8 | Nov 2024 | Colt-RMZ JV | Colt DCS + RMZ Corp | $1.7B | JV | 250+ MW | Real estate meets DC |

| 9 | 2024 | CapitaLand Fund | CapitaLand Investment | S$150M | Fund | 200+ MW | First India-dedicated |

| 10 | Jan 2025 | AWS India | AWS | $12.7B | Captive+Colo | 500+ MW | Largest hyperscaler |

| 11 | Feb 2025 | Microsoft Azure | Microsoft | $17.5B | Captive+Colo | 300+ MW | Cumulative commitment Dec 2025, covering cloud + AI infrastructure 2025-2029 |

| 12 | Jul 2025 | Google-Adani | Google + AdaniConneX | $15B | JV/Captive | 1 GW | Largest DC project |

| 13 | Jul 2025 | EverYondr restr. | Everstone ← Yondr | Undisclosed | Buyout | 100 MW | Yondr exits |

| 14 | Aug 2025 | Sify IPO | Sify Technologies | $500M | IPO prep | 188 MW | Pure-play DC IPO |

| 15 | Nov 2025 | Digital Connexion | Reliance+Brookfield+DR | $11B | JV | 1 GW | Triple-party JV |

| 16 | Dec 2025 | CapitaLand-CLINT | CIDCF ← CLINT | S$99.7M | Fund acq | 3 fac. | Fund deploys capital |

Source: Company announcements; Bloomberg; DCD; Houlihan Lokey Dec 2025; IDCR 2026 compilation

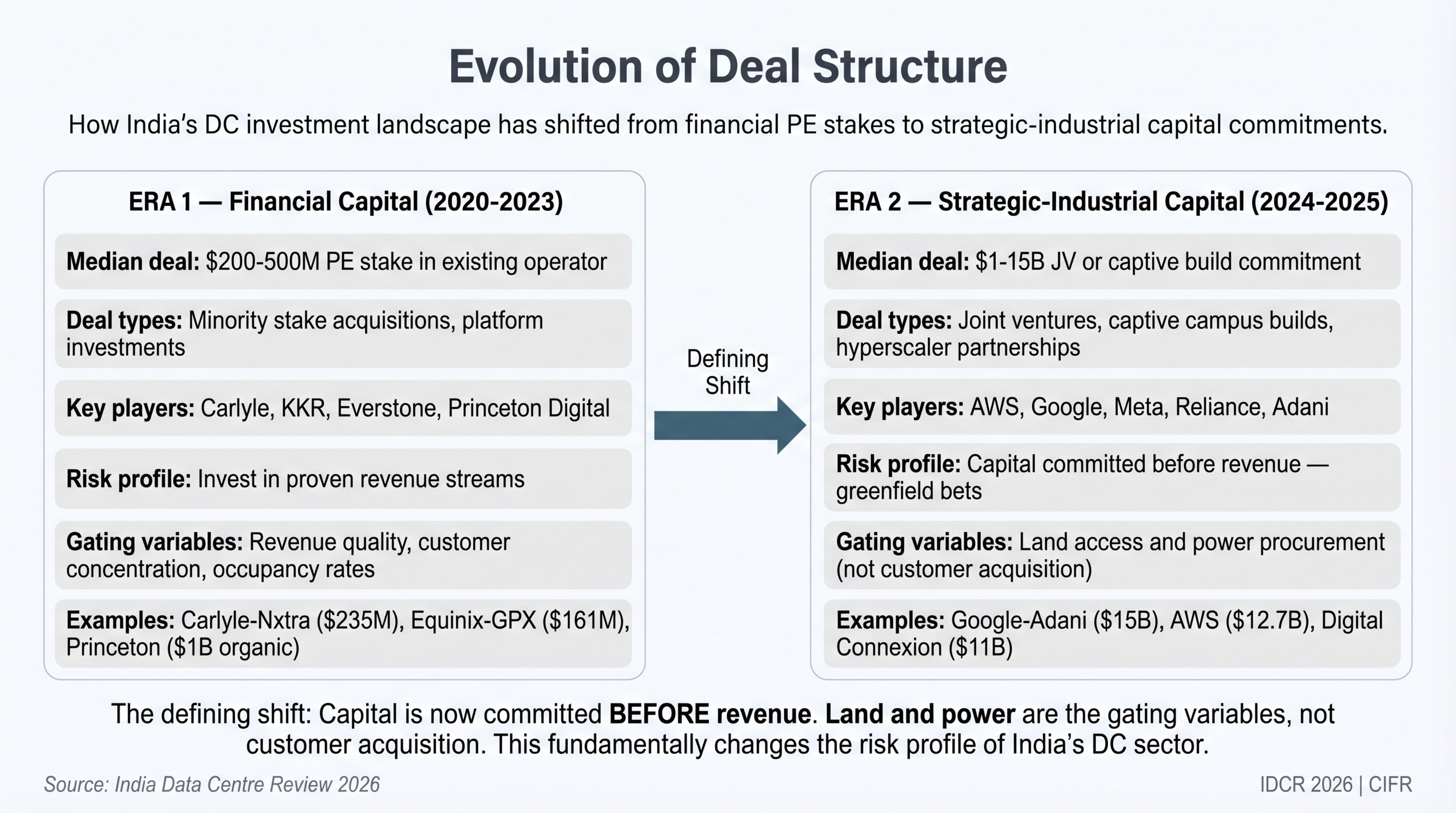

India's DC investment landscape shifted from financial investors to strategic-industrial capital. From 2020-2023, median deal size was $200-500M PE stakes in existing operators. In 2024-2025, the median deal scaled to $1-15B joint-venture or captive builds.

This restructuring changes risk: capital commits before revenue, with land and power as primary gating variables instead of customer acquisition. Hyperscaler commitments (AWS $12.7B, Google-Adani $15B, Microsoft $17.5B) signal long-term, infrastructure-grade investment.

Keep reading — free, takes 30 seconds

Investment Flows, Deal Tracker, and Financial Benchmarks continues with 1,292 words and 12 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.