Operator Landscape and Competitive Dynamics

How a dozen operators are shaping a $7B market — and who has the structural advantage.

Live operator-relevant context: day-ahead price · live capex landscape at /data-centres · operator economics commentary in /insights.

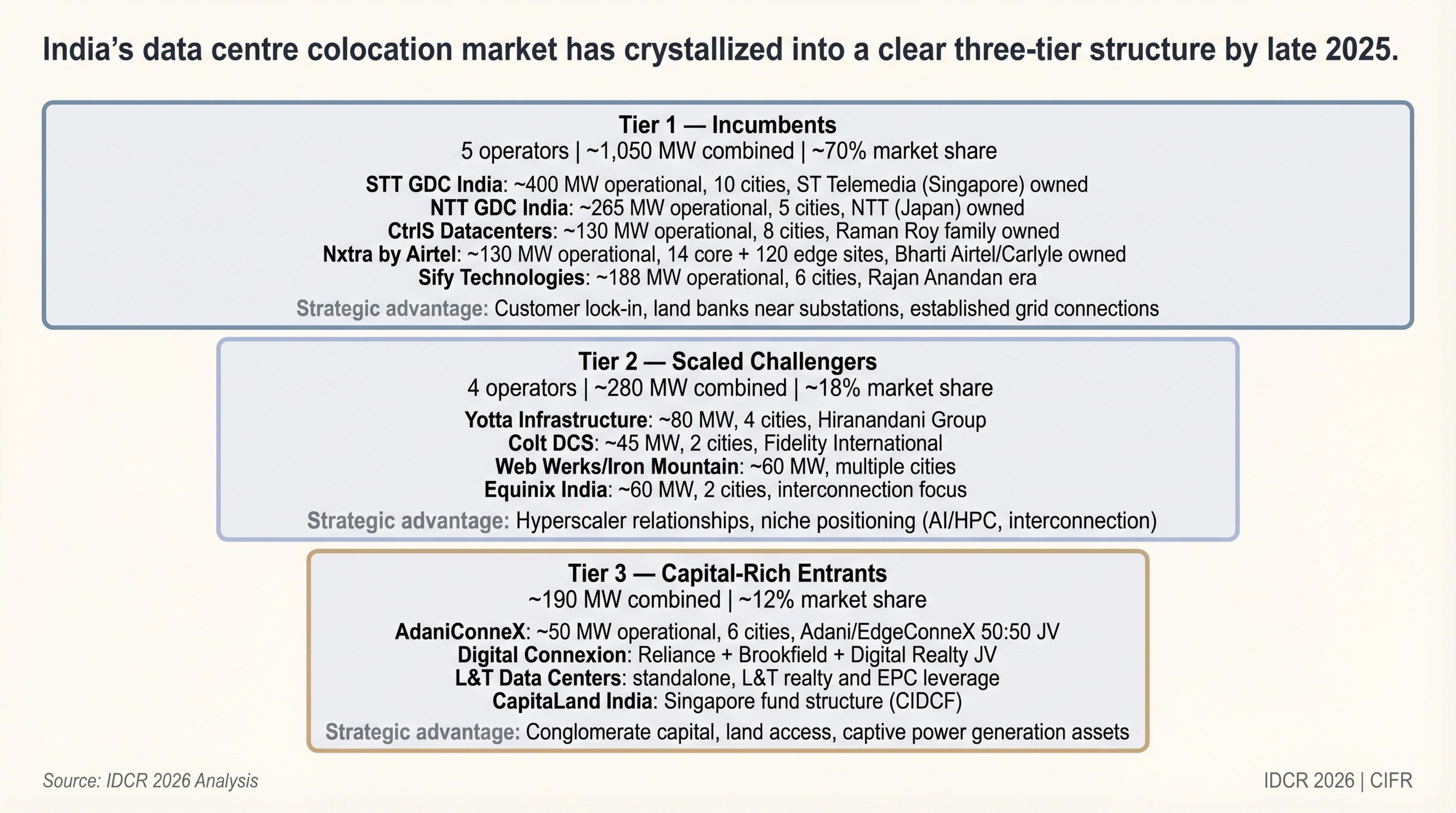

India's DC Market Has Crystallized into Three Distinct Tiers

India's colocation market has crystallised into a three-tier structure by late 2025 (Houlihan Lokey· Houlihan LokeyDec 2025; Cushman & Wakefield· C&WH1 2025). Tier 1 incumbents control ~75% of operational capacity through five operators: STT GDC (400 MW, see Maharashtra/Karnataka), NTT (265 MW, primarily Mumbai), CtrlS (130 MW, Hyderabad-led), Nxtra (130 MW, pan-India), and Sify (188 MW, Noida-led). Tier 2 comprises scaled challengers with 30--80 MW each: Yotta, Colt DCS, Web Werks/Iron Mountain, and Equinix. Tier 3 entrants---AdaniConneX, Digital Connexion (Reliance--Brookfield--Digital Realty), and CapitaLand---bring conglomerate capital but limited operational deployment so far.

| Three-Tier Market Structure | ||||

|---|---|---|---|---|

| Tier | Operators | Combined Capacity | Market Share | Strategic Advantage |

| Tier 1 — Incumbents | STT GDC, NTT, CtrlS, Nxtra, Sify | 1,050 MW | 70% | Customer lock-in, land banks, grid connections |

| Tier 2 — Scaled Challengers | Yotta, Colt DCS, Web Werks/Iron Mountain, Equinix | 280 MW | 18% | Hyperscaler relationships, niche positioning |

| Tier 3 — Capital-Rich Entrants | AdaniConneX, Digital Connexion, CapitaLand | 190 MW | 12% | Conglomerate capital, land access, energy assets |

Source: IDCR 2026 estimates based on Houlihan Lokey Dec 2025; company disclosures; CBRE H2 2025

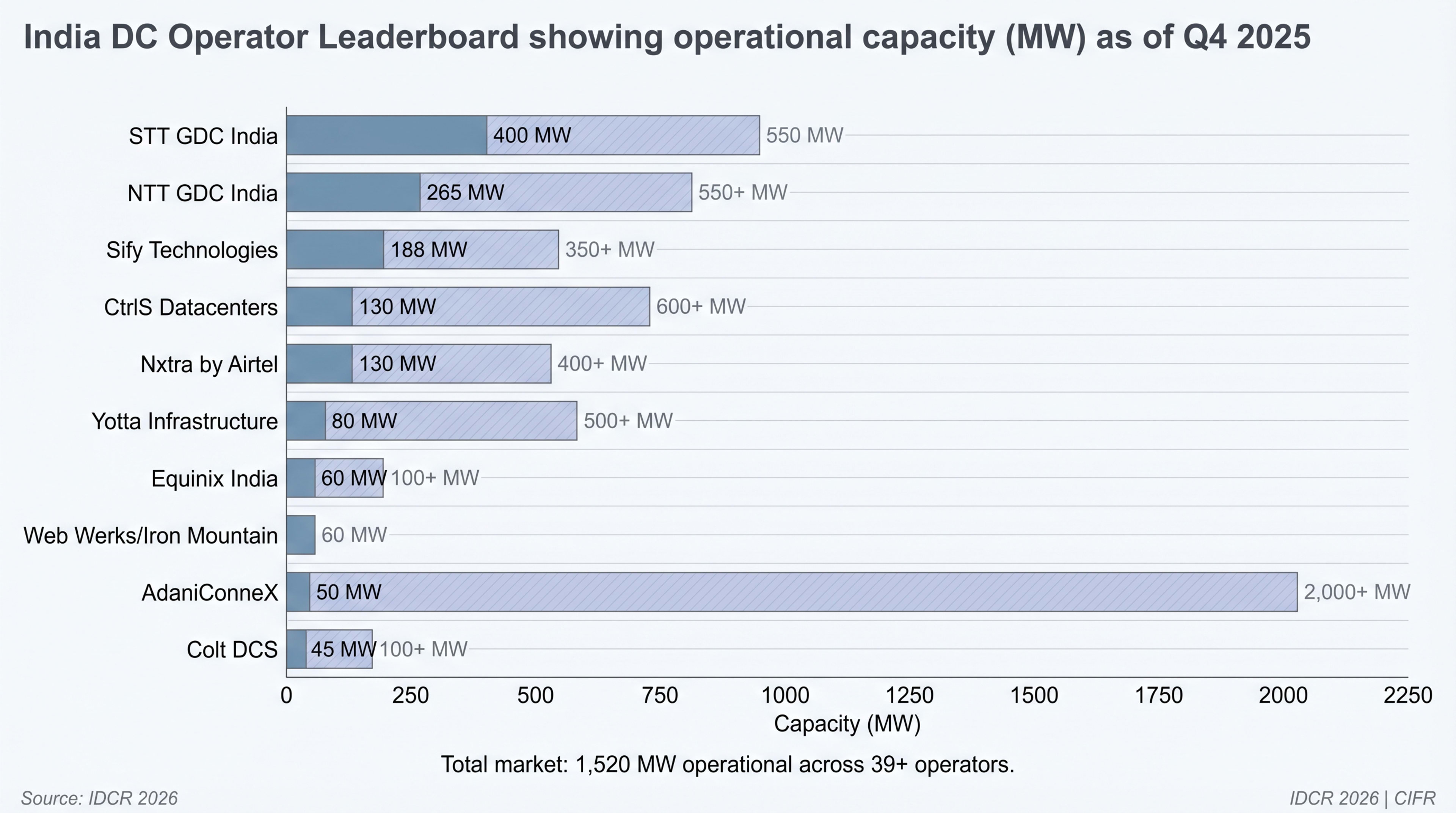

STT GDC Leads on Installed Base, but NTT and Nxtra Are Closing the Gap

| India DC Operator Leaderboard — Operational Capacity (Q4 2025) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Rank | Operator | Ownership | Operational MW | Pipeline MW | Cities | Key Clients | Revenue (est.) | Expansion Highlight |

| 1 | STT GDC India | ST Telemedia (Singapore) | 400 | 550 | 10 | Hyperscalers, BFSI | $450M (28% share) | $3.2B for 550 MW over 5–6 yrs |

| 2 | NTT GDC India | NTT (Japan) | 265 | 550+ | 5 | Cloud, BFSI, Govt | $320M ( 20% share) | 400 MW Hyderabad AI campus; $1.2B committed |

| 3 | CtrlS Datacenters | Raman Roy family | 130 | 600+ | 8 | BFSI, Pharma, IT | ₹1,567 Cr ( $185M) | 612 MW Hyderabad mega-campus |

| 4 | Nxtra by Airtel | Bharti Airtel / Carlyle | 130 | 400+ | 14 core + 120 edge | Airtel captive, Cloud | $150M (15% share) | $1B fundraise; 1 GW target in 3–4 yrs |

| 5 | Sify Technologies | Rajan Anandan era | 188 | 350+ | 6 | IT Services, Cloud | $140M (est.) | Noida 02 hyperscale; INR 3,000 Cr investment |

| 6 | Yotta Infrastructure | Hiranandani Group | 80 | 500+ | 4 | AI/HPC, Govt, Cloud | $100M (est.) | $2B Nvidia AI hub partnership; FY27 IPO planned |

| 7 | Equinix India | Equinix (US) | 60 | 100+ | 2 | Interconnection, Fintech | Not disclosed | Chennai IBX launched Sep 2025 |

| 8 | AdaniConneX | Adani/EdgeConneX 50:50 | 50 | 2,000+ | 6 | Hyperscalers (Google) | Early-stage | $15B Google Vizag partnership; 5 GW target |

| 9 | Colt DCS | Fidelity International | 45 | 100+ | 2 | Enterprise, Fintech | Not disclosed | Mumbai, Navi Mumbai expansion |

Source: Company disclosures; Houlihan Lokey Dec 2025; ICRA Sep 2025; Blackridge Research Feb 2026. Revenue estimates are IDCR 2026 approximations based on publicly available data and may differ from audited figures.

Note: Operational capacity figures in this table represent IT load capacity as reported by Cushman & Wakefield H1 2025 and operator disclosures. Company-reported figures may include capacity under commissioning or use total facility power definitions that yield higher numbers. Where discrepancies exist with company claims, we note the difference.

Hyperscalers Commit $45.2B to DC Infrastructure — Bifurcating Demand

Hyperscalers shifted decisively towards captive and JV builds in 2025, anchored by four major commitments:

- AWS: $12.7B (by 2030) for 500+ MW, primarily Mumbai-focused, via partnerships with NTT and STT GDC.

- Microsoft: $17.5B (2025–2029) for 300+ MW cloud and AI infrastructure, including a new Hyderabad region (mid-2026).

- Google: $15B for a 1 GW Visakhapatnam AI Hub with AdaniConneX (see Chapter 4, Deal #12).

- Meta/Reliance: $12–15B for 1 GW AI capacity as a joint venture.

Colocation remains essential for interconnection-heavy workloads, network peering, and regional edge presence. IDCR estimates 40--50% of hyperscaler pipeline capacity will flow through colocation partnerships; the remainder pursues pure captive builds.

| Hyperscaler India Commitments (as of March 2026) | ||||

|---|---|---|---|---|

| Hyperscaler | Total Commitment | Primary Model | Key Partners | **Target Capacity |

| AWS | $12.7B by 2030 | Captive + Colo | NTT, STT GDC | 500+ MW |

| Microsoft | $17.5B | Captive + Colo | STT, CtrlS, Sify | 300+ MW |

| $15B (Vizag) | JV (AdaniConneX) | AdaniConneX | 1 GW | |

| Meta/Reliance | $12–15B | JV | Reliance Jio | 1 GW |

| Digital Connexion | $11B | JV (Reliance-Brookfield-Digital Realty) | Equal thirds | 1 GW (Vizag) |

Keep reading — free, takes 30 seconds

Operator Landscape and Competitive Dynamics continues with 1,450 words and 17 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.