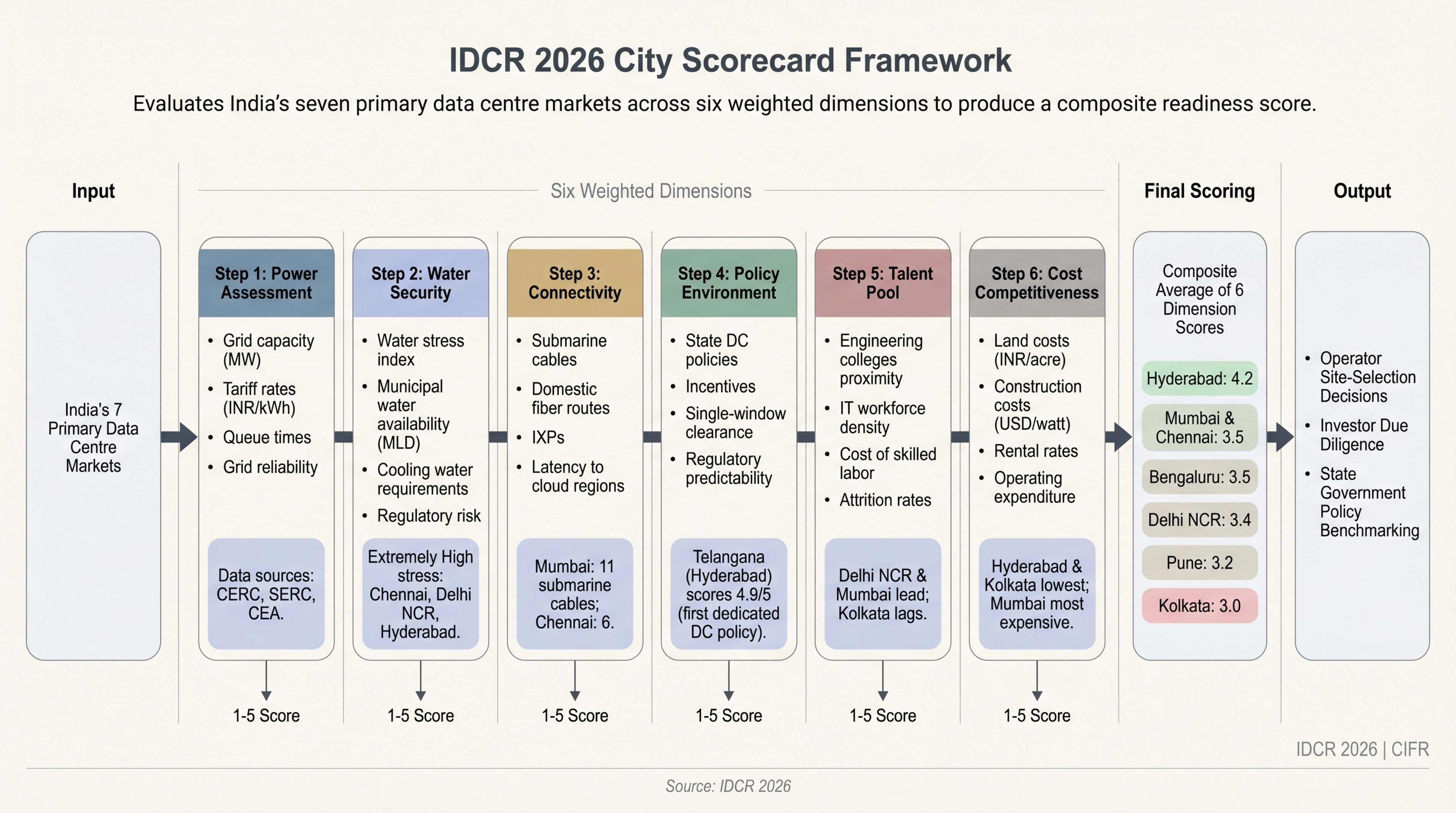

City-Level Deep Dives: Seven Markets Dissected

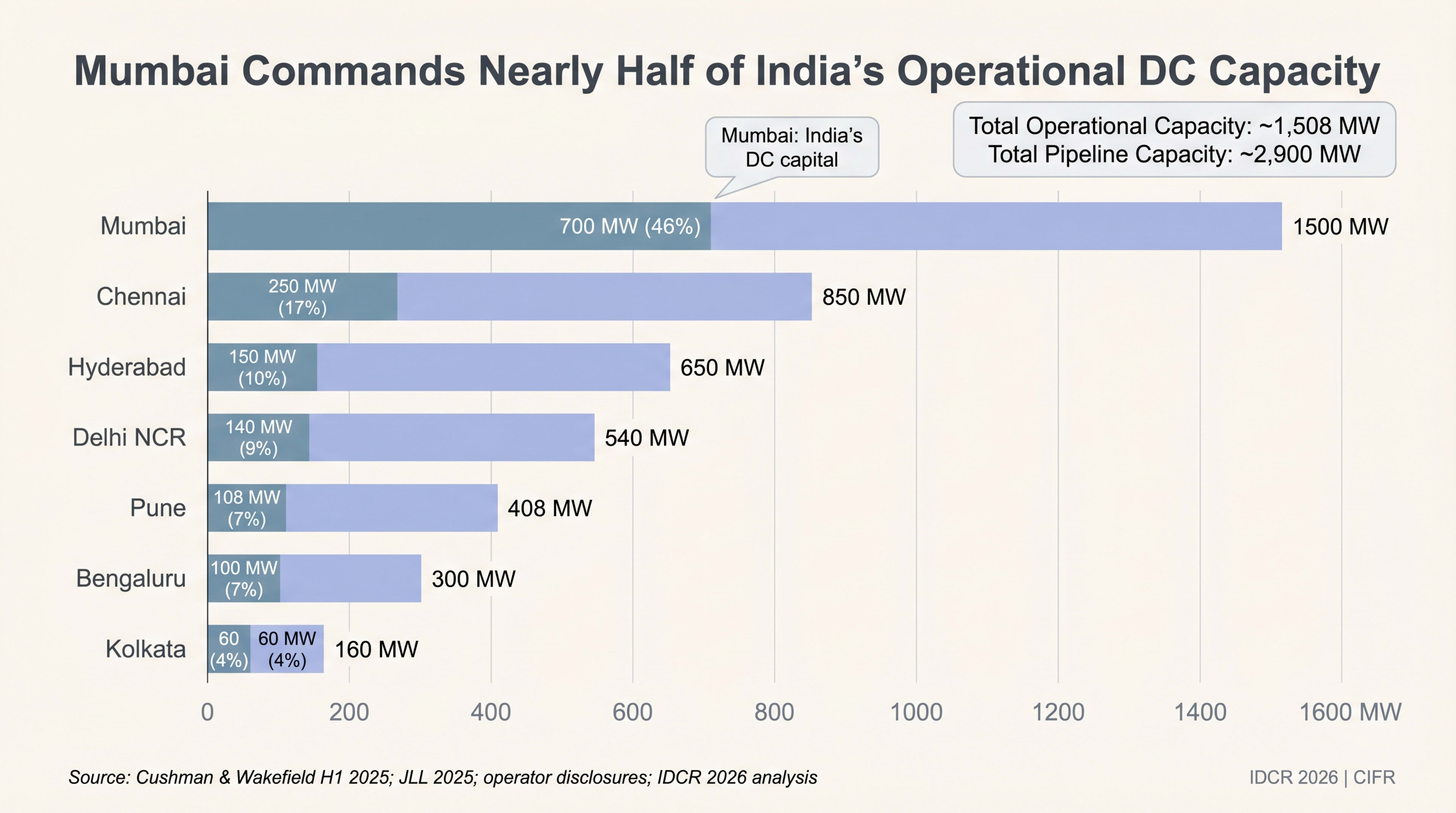

India's data centre capacity is concentrated in seven cities that collectively account for 97% of operational capacity, but the geographic distribution is shifting rapidly. Mumbai commands 54% of national capacity through legacy infrastructure and submarine cable dominance, yet its share is declining as power constraints, water stress, and high costs drive operators to secondary markets. Hyderabad has emerged as the fastest-growing hub with an 8x pipeline-to-operational ratio, powered by Telangana's pioneering data centre policy. Chennai leverages six submarine cable systems as India's second international gateway. This chapter dissects each market across six dimensions — power, water, connectivity, policy, talent, and cost — providing a city-level scorecard framework, micromarket analysis within each hub, and an investor decision matrix for city selection by workload type, risk appetite, and capital size. The central thesis: India's data centre geography is deconcentrating along the same trajectory that took the US market from Northern Virginia dominance to a distributed national footprint, but compressed into a shorter time horizon.

Live state demand: Maharashtra · Tamil Nadu · Telangana · Karnataka · Uttar Pradesh · Gujarat · West Bengal. Compare grid context across markets at /compare.

Market Overview

India's data centre market is concentrated in seven cities that collectively account for 97% of operational capacity. This chapter dissects each market, revealing distinct competitive dynamics, regulatory environments, and growth trajectories. From Mumbai's dominance constrained by geography to Hyderabad's rapid rise powered by enlightened policy, these markets represent the geographic and strategic divide shaping India's digital infrastructure investment.

The geographic concentration in these seven cities reflects cumulative infrastructure investment dating back over two decades. Mumbai emerged as the natural entry point for hyperscalers due to its position as India's primary international gateway: eleven submarine cable systems land in Mumbai, a legacy of the city's colonial-era port infrastructure and continued position as India's financial capital. Chennai similarly benefited from six submarine cable landings, creating a secondary gateway for APAC-bound traffic. Hyderabad's rise, by contrast, is policy-driven rather than geography-driven, enabled by Telangana's 2016 Data Centre Policy which offered power subsidies, land acceleration, and tax incentives that no other state could match at that time. Delhi NCR captured the northern enterprise market through proximity to India's largest IT services cluster (Delhi has 800,000+ IT professionals) and its role as the seat of government, driving demand from government ministries and national BFSI leaders.

What began as concentration around submarine cable landing points and legacy enterprise clusters is now experiencing structural deconcentration. This deconcentration thesis rests on three observations: (1) Hyperscaler platform economics have changed: cloud platforms deploy in low-cost greenfield sites provided power is abundant and latency meets workload requirements (50-100 ms for training, 200+ ms for batch jobs); AI/ML training and inference can be served from lower-cost, greenfield sites provided power is abundant and latency is manageable (50-100 ms for training, 200+ ms for batch jobs); (2) Abundant power supply and low tariffs now drive site selection more than submarine cable proximity: an 18-month grid queue in Mumbai and 8-12 month delays in Chennai mean that even well-capitalized operators cannot scale, whereas Hyderabad and emerging markets can deploy 100+ MW within 12 months; (3) State policy has become as important as geography: Telangana's power subsidies (INR 5-6/kWh vs INR 8-10/kWh in Mumbai) create a 30-40% cost advantage that compounds over a 25-year facility life, justifying the shift of new capacity to lower-cost regions even if they lack direct submarine cable access.

The historical precedent is US market deconcentration from Northern Virginia (D.C. data centre hub: 40% of US colocation capacity by 2010) to secondary markets (Dallas, Phoenix, Oregon). Over the 2010-2025 period, Northern Virginia's share declined from ~40% to ~28%, as hyperscalers and enterprises discovered that content delivery networks, fiber density improvements, and cloud architecture eliminated the strict need for presence in the legacy hub. India will follow a similar path, albeit compressed into a shorter time horizon. Mumbai is likely to decline from today's 54% of national capacity to 35-40% by 2030, with Hyderabad, Chennai, and Pune capturing the incremental capacity build-out (IDCR 2026 projections).

The evolution can be segmented into four phases: (1) Emergence (2010-2014) with small hyperscaler-focused deployments; (2) Standardization (2015-2017) driven by enterprise demand; (3) Consolidation (2018-2021) with global operators entering; and (4) Expansion (2022-2026) driven by cloud adoption, AI workloads, and regional diversification.

Keep reading — free, takes 30 seconds

City-Level Deep Dives: Seven Markets Dissected continues with 7,099 words and 14 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.