Policy and Regulatory Landscape

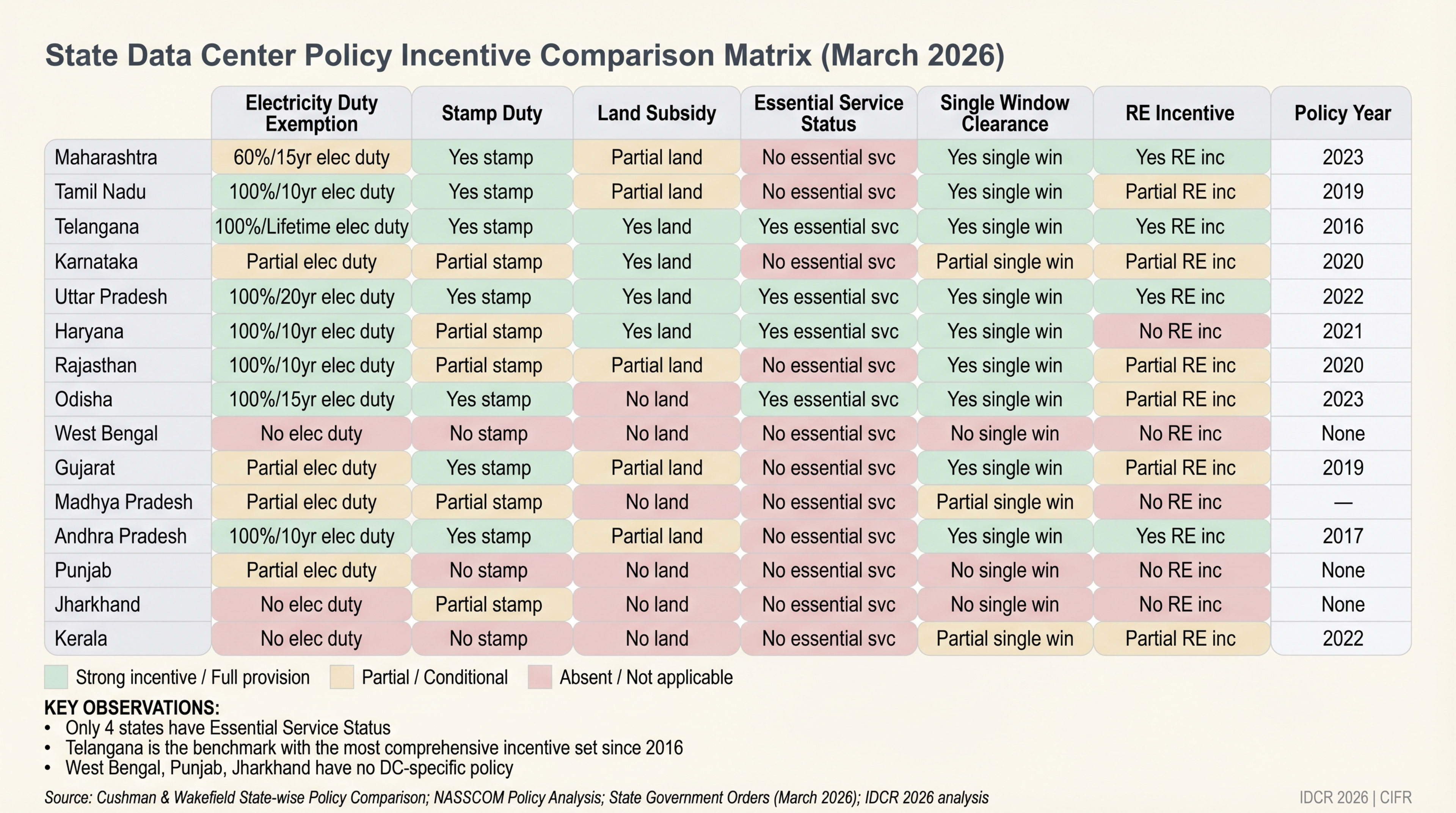

India has 15+ state data centre policies and a draft national framework — operators still navigate 30+ approvals to build a single facility.

Atlas reference for DC policymaking: state regulatory pages at /regulatory · per-state tariffs and DC exemptions at /tariffs · all 36 state pages indexed at /states.

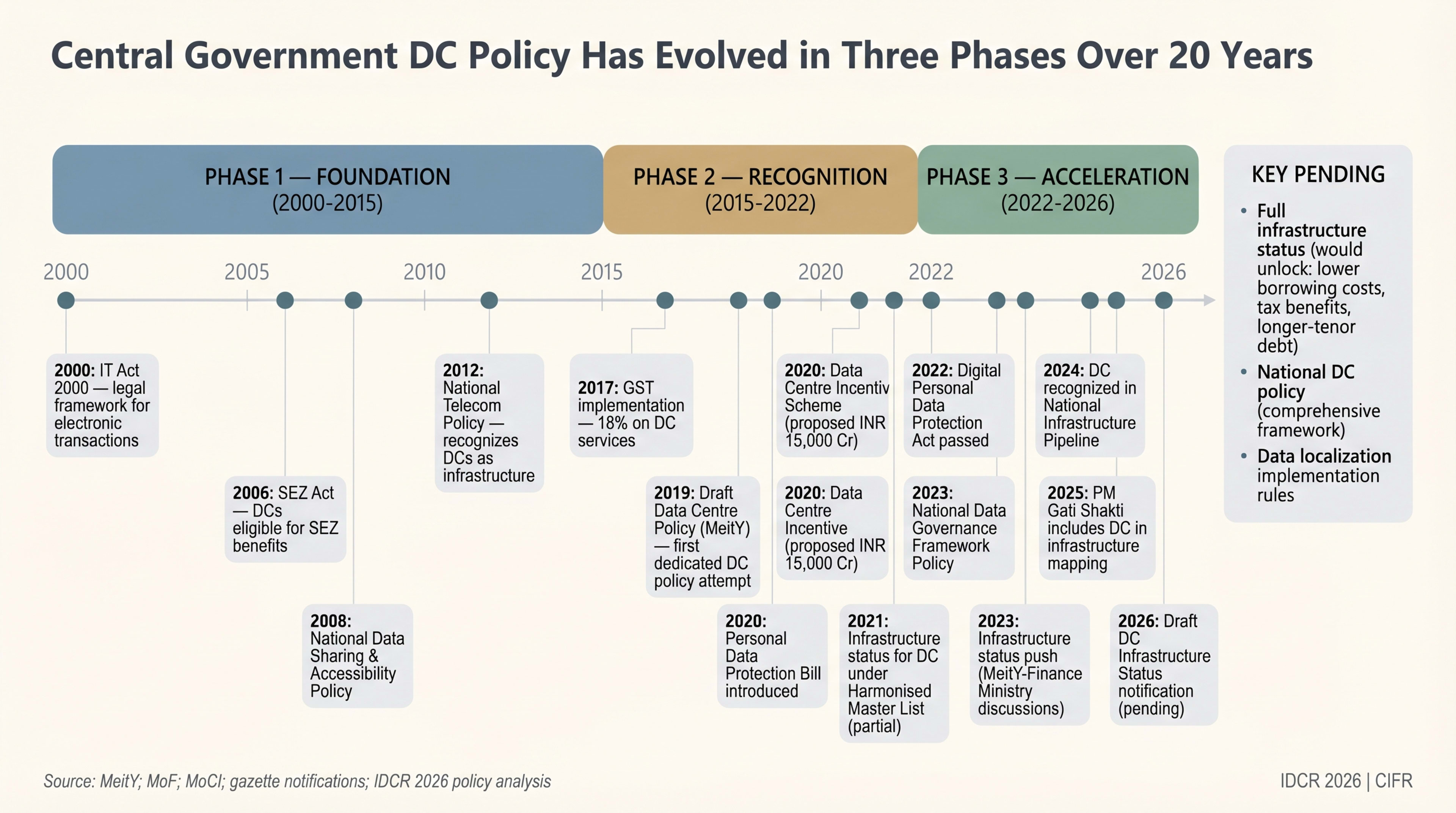

A National Data Centre Policy, Five Years in the Making, Finally Takes Shape

India's data centre sector has reached $10 billion in market value (Houlihan Lokey· Houlihan LokeyDec 2025). The Draft National Data Centre Policy, first announced in 2020 but shelved repeatedly, was revived by MeitY· MeitYSep 2025 in September 2025 and placed under stakeholder consultation. Compare state policies live at Maharashtra, Telangana, Tamil Nadu, Karnataka, UP, and Gujarat.

As of March 2026, the final policy has not been gazetted. The draft contains five provisions that would reshape the sector's economics.

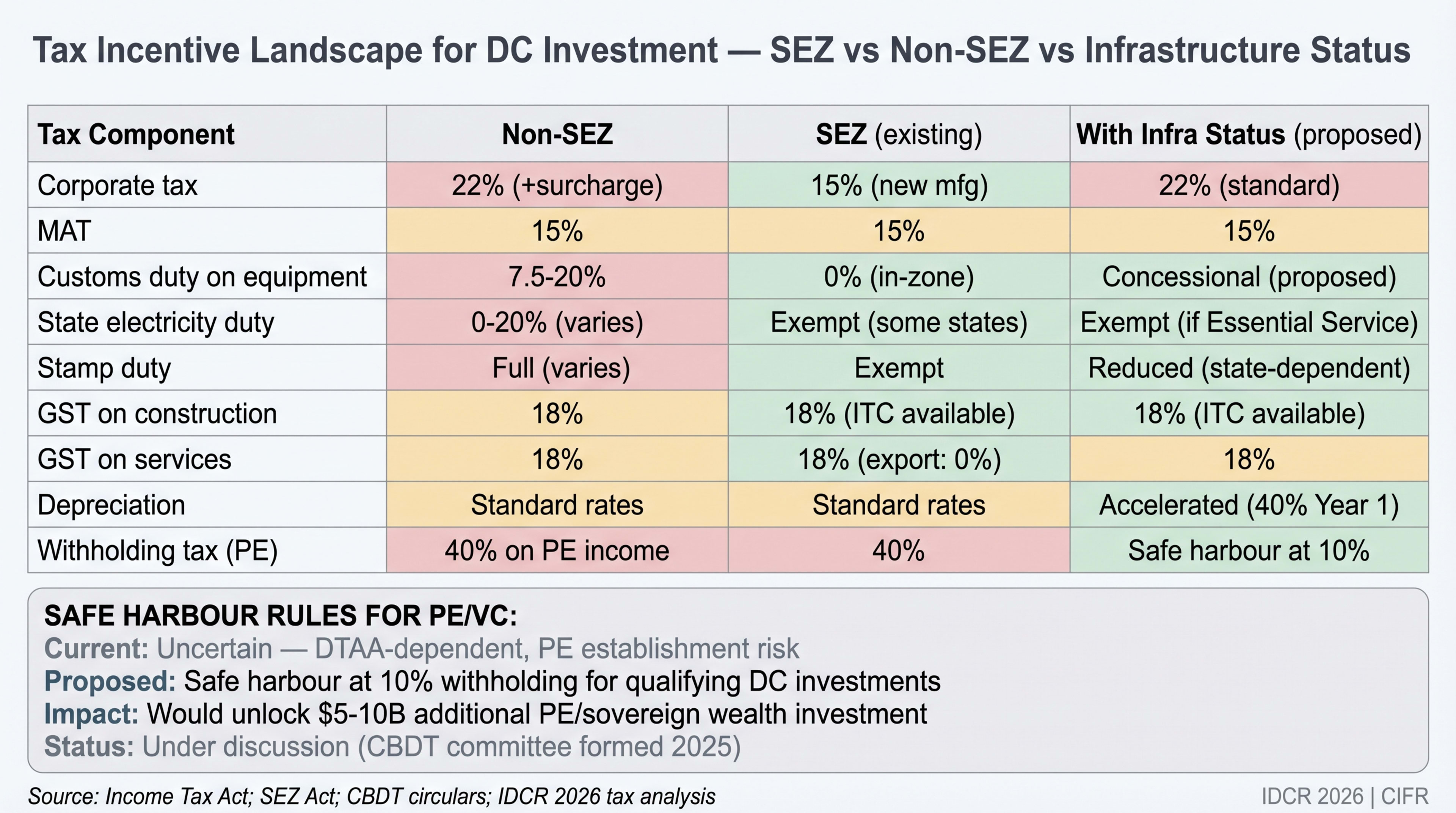

- Conditional tax exemptions of up to 20 years for operators meeting capacity addition, PUE, and employment targets.

- GST input tax credits on capital assets (HVAC, electrical, cooling). If granted, effective construction costs could fall by 12–18%, addressing a long-standing industry demand.

- 100% electricity duty exemption at the central level.

- Data Centre Economic Zones (DCEZs) with pre-allocated land near industrial corridors and IT hubs.

- Single-window clearance mechanism to replace the current 30+ approval process.

Operators welcome the tax and GST provisions. However, earlier versions (2020, 2022) never progressed beyond draft. The DCEZ concept lacks implementation detail: no specific zones have been identified, and the land allocation mechanism is undefined. Single-window clearance faces the same state-centre coordination challenge that has stalled other Indian infrastructure initiatives.

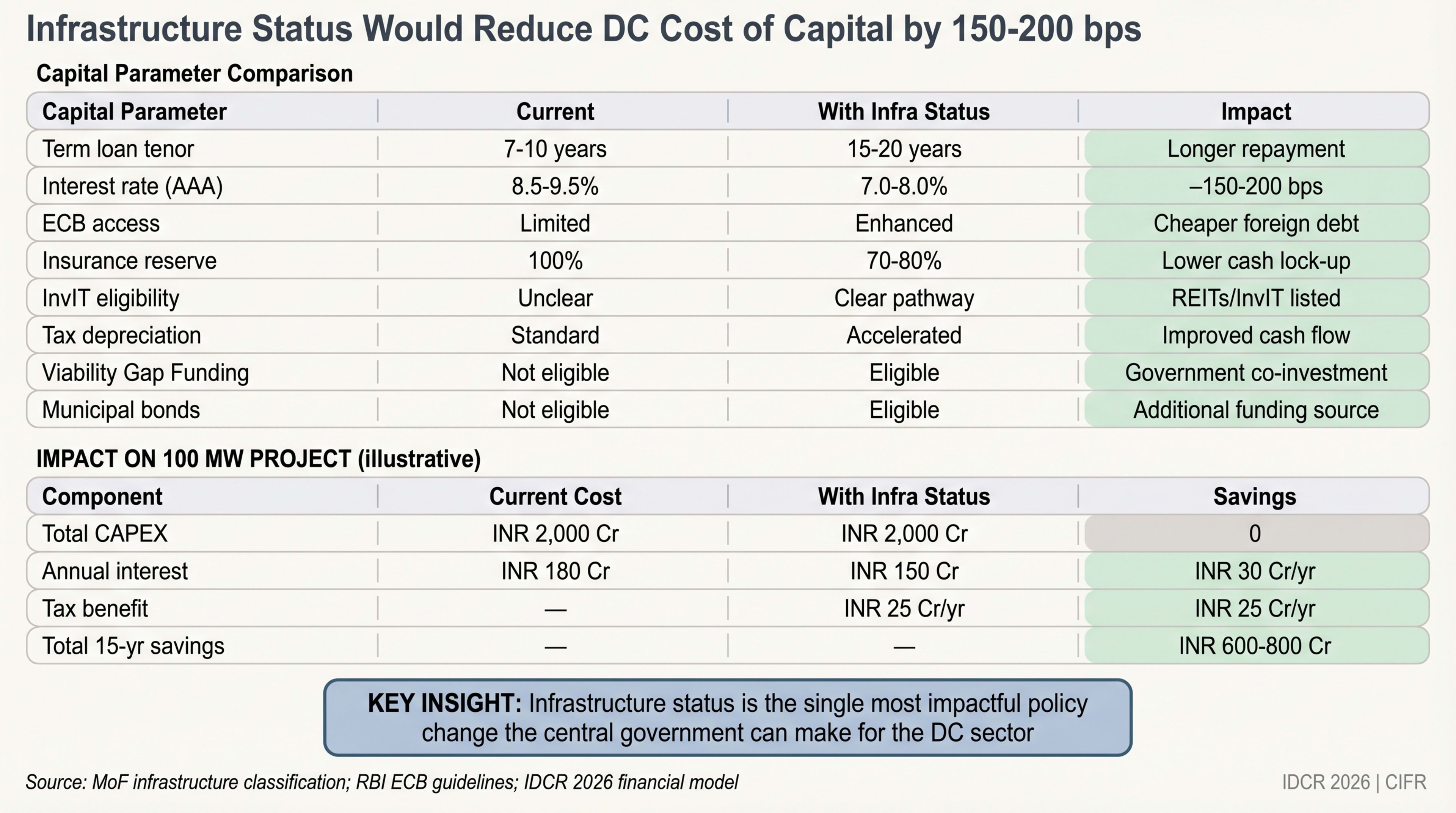

The Draft National Data Centre Policy's most consequential provision may be infrastructure status for data centers. If granted, this would allow operators to access long-tenor debt from insurance companies and pension funds at lower interest rates, fundamentally altering the capital structure of Indian DC projects. Currently, Indian operators rely primarily on bank debt and private equity --- infrastructure status would open the institutional debt market and compress the cost of capital by an estimated 100--200 basis points.

Keep reading — free, takes 30 seconds

Policy and Regulatory Landscape continues with 2,632 words and 12 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.