Demand Drivers: AI, Cloud, 5G, and Digital Consumption

How AI inference, cloud migration, 5G edge deployments, and digital consumption compound into non-linear data centre demand — and why the ceiling keeps moving.

Four concurrent technology waves are compounding to produce the most sustained data center demand cycle in India's digital history. Understanding their individual and combined effects is essential for capacity planning through 2030.

Atlas context for demand: national load forecasts at /forecast · live DC-relevant grid context at /data-centres · cross-cutting analysis at /insights.

AI and Machine Learning Will Consume 30% of India's DC Capacity by 2027

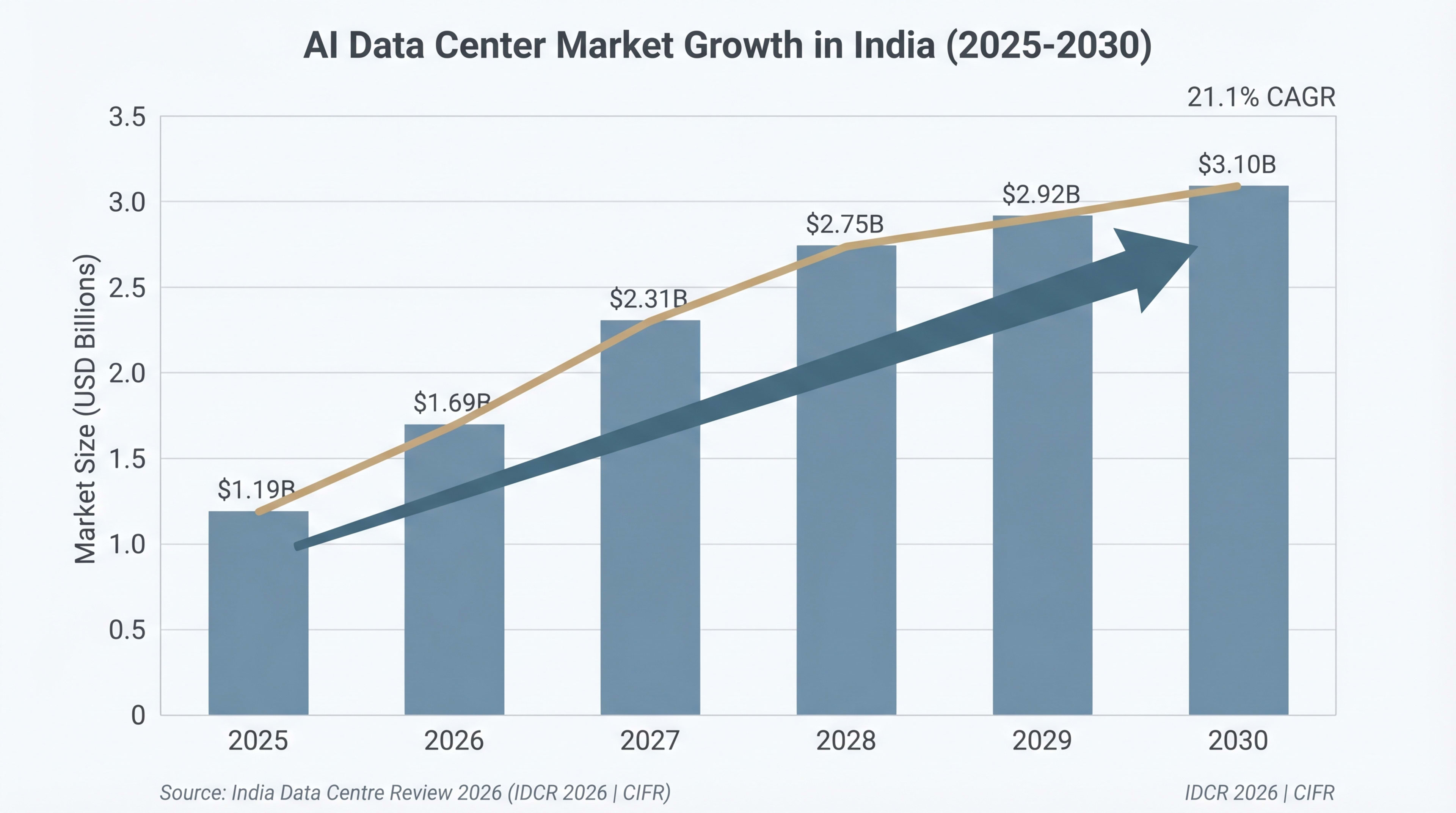

Artificial intelligence is reshaping India's data centre industry. The India AI-optimised data centre market, valued at $1.19 billion in 2025, is projected to reach $3.10 billion by 2030, expanding at a 21.1% CAGR (Mordor Intelligence· Mordor Intelligence2025). State-level AI clusters are concentrating in Telangana, Karnataka, and Tamil Nadu; the L&T-NVIDIA AI factory adds a Mumbai node. This expansion represents a structural shift in the type, density, and economics of data centre capacity the market requires.

GPU-dense deployments mark the inflection point. A single AI training rack consumes 40--80 kW, compared with 6--8 kW for a conventional enterprise compute rack --- a five- to ten-fold increase in power density. This density increase reshapes cooling architecture, power distribution, and facility design. Existing infrastructure built for conventional workloads now requires significant retrofitting to accommodate the power and thermal demands of modern AI clusters.

India's national compute infrastructure has scaled faster than originally planned. The IndiaAI Mission, approved in March 2024 with a Rs 10,372 crore (~$1.14 billion) outlay, initially targeted 10,000 GPUs. By mid-2025, deployment reached approximately 34,000 GPUs, and IT Minister Ashwini Vaishnaw announced at the India AI Impact Summit in February 2026 that an additional 20,000 GPUs were approved for procurement --- targeting approximately 58,000 GPUs (Source: PIB June 2025; Organiser February 2026). The programme offers 40% capital subsidy on GPU procurement (Source: PIB, June 2025; Organiser, February 2026).

Private-sector GPU deployments are accelerating alongside the government programme. Yotta Data Services has ordered more than 16,000 NVIDIA H100 GPUs for its Shakti Cloud platform, with plans to scale to 32,768 units. In February 2026, Larsen & Toubro partnered with NVIDIA to build a sovereign AI factory, expanding a 30 MW GPU compute cluster in Chennai and launching a 40 MW AI-ready facility in Mumbai. OpenAI signed as the first customer of Tata Consultancy Services' data centre business, contracting for 100 MW with an option to scale to 1 GW (Source: CNBC, February 2026; EE Times, February 2026).

| AI/GPU Infrastructure Initiative | Capacity | GPU Count | Investment | Status |

|---|---|---|---|---|

| IndiaAI Mission (Government) | — | 38,000+ | $1.14B | Operational |

| Yotta Shakti Cloud | — | 16,000+ | $2.0B | Scaling |

| L&T + NVIDIA AI Factory (Chennai + Mumbai) | 70 MW | — | — | Announced Feb 2026 |

| TCS DC (OpenAI as anchor tenant) | 100 MW–1 GW | — | — | Contracted |

| Google + Adani Cloud Regions | 80 MW (Phase 1) | — | $15B | Mid-2026 |

Source: Compiled from PIB, CNBC, EE Times, company announcements, February 2026

India's GPU compute capacity has already exceeded original IndiaAI Mission targets by 3.8x, reaching 34,000+ GPUs against a 10,000-unit plan. With 20,000 additional GPUs planned for 2026 and private-sector clusters scaling independently, India is building the computational substrate for a domestic AI ecosystem --- but power and cooling infrastructure must keep pace with rack densities that are 5--10x higher than conventional workloads.

The India Semiconductor Mission adds a second dimension to AI demand. The Semicon India Programme has attracted approximately Rs 1.6 trillion (~$17.3 billion) in investment commitments across ten sanctioned projects. Tata Electronics and Taiwan's PSMC are building a $10.9 billion fabrication plant in Dholera, Gujarat, targeting first silicon by late 2026. Micron's $2.75 billion assembly and test facility in Sanand, Gujarat began commercial production in February 2026 (Source: Carnegie Endowment, August 2025; India Briefing, 2025).

Semiconductor fabrication plants are not data centres, but they generate enormous test-and-validation compute demand. More significantly, they signal India's intent to build end-to-end AI value chains --- from chip fabrication through training infrastructure to inference at the edge.

Keep reading — free, takes 30 seconds

Demand Drivers: AI, Cloud, 5G, and Digital Consumption continues with 2,225 words and 18 figures.

Free Clerk account. No card. We use it to remember your reading position and unlock subscriber chapters.